Seed Funded Research: Impact of media on real estate markets: media coverage identification and machine learning in news articles.

Seed Funded Research: Impact of media on real estate markets: media coverage identification and machine learning in news articles.

A core strategy of the Reading Real Estate Foundation (RREF) is to support and nurture the advancement of research in the sphere of Real Estate. We undertake this by funding two key initiatives, PhD Scholarships and RREF Seed Funding, to foster innovation at the Department of Real Estate and Planning, Henley Business School, a globally renowned centre for teaching and research excellence.

Recently, RREF caught up with two of academics from the department, Dr Yi Wu and Dr Steven Devaney, who received funding from the RREF Seed Fund to pursue their research; 'Impact of media on real estate markets: media coverage identification and machine learning in news articles'.

Why is funding like the Seed Fund important to researchers and their projects?

Without seed funding it can be hard to test and demonstrate whether new research methods are likely to be successful. Our proposed methods were novel, but they required significant levels of data collection that needed to be resourced, and for which external funding was difficult to obtain in the absence of scoping whether the techniques could work. The seed funding therefore accelerated the development of this research by enabling us to test the feasibility of our methods. This established our confidence for preparing a research proposal for externally funded follow-on work. Moreover, it provided experience of academic fieldwork to our research assistants, who played an important role in our research team.

Can you tell us more about the funded research and it's potential impact for the industry?

This project investigates whether the media has an impact on real estate market pricing and performance. We build on literature about the impact of sentiment on real estate (e.g., Ling, Naranjo and Scheick, 2014; Marcato and Nanda, 2016; Freybote and Seagraves, 2017). Those studies focused on market-level outcomes, but we are examining the impact of news headlines and articles on individual deals and companies. We also contribute to the literature by analysing sentiment from articles by real estate news providers rather than just financial news providers (Hausler, Ruscheinsky and Lang, 2018; Ploessl, Just and Wehrheim, 2021).

There are two components to this project. One is the investigation and classification of news suppliers in an existing database (RavenPack) that provides sentiment scores for individual articles. This supports our investigation of the impact of news media on pricing in private CRE markets using this database and transaction data supplied by Real Capital Analytics. The other is examination of UK real estate news providers and the development of sentiment scores for REITs based on articles about those firms. It will provide new evidence on how the perception of real estate company activities affects stock performance and therefore company value.

What was the impact of receiving this funding for your research?

The funding helped us recruit two research assistants for data collection on the nature of media outlets that produce news, which has developed into a more comprehensive media supplier characteristic dataset. This dataset will contribute to our analysis of private CRE transactions, which has the provisional title: Does positive media coverage influence the trading activity and bargaining power of CRE investors? We believe this will facilitate publication in a leading real estate journal or a finance journal. The finance literature now includes many articles based on analysis of sentiment based on media, but it remains a novel area of investigation in relation to real estate.

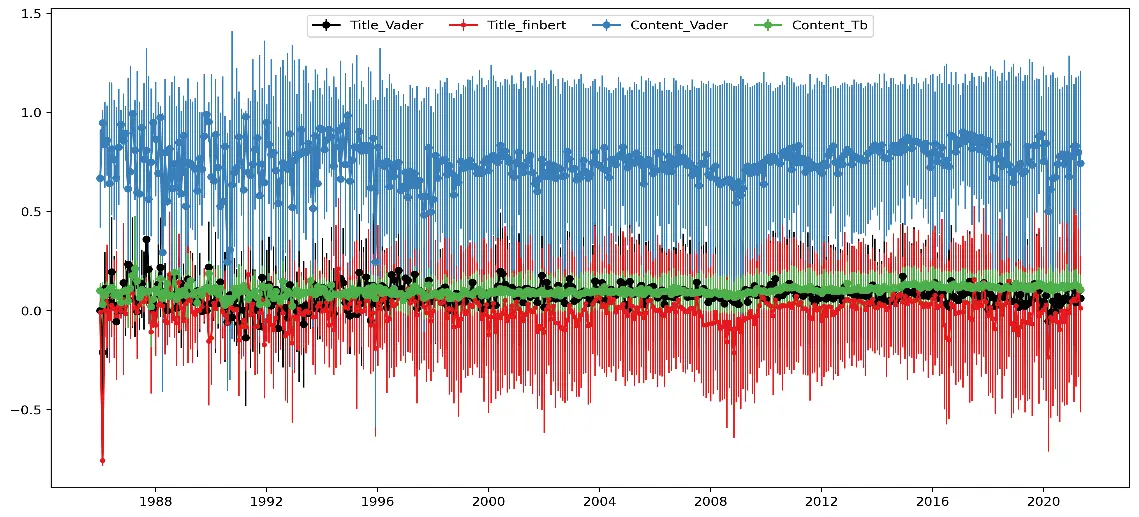

The funding also supported recruitment of a research assistant for textual analysis of a pool of UK real estate articles. They downloaded a sample of articles related to 32 UK REITs from EG News and Property Week and produced a time series of sentiment scores using the TB, Vader and Finbert textual analysis packages. The graph below provides a comparison of the different approaches. Although the signals are noisy, the rises and falls mirror the UK real estate market cycle in this period.

Graph: Time series graphs by comparing different sentiment score of title and content from property week and EGI

These measurements of sentiment towards individual companies are novel of themselves, but they also provide us with the platform for analysing how the perception of company activities affects stock performance and company value.

How has the funding supported future development of this research?

The funding in support of the textual analysis / machine learning proved the feasibility of our methodology and gave us confidence to develop an application for external funding from the 2022 EPRA Research Programme. (This is still under consideration, with a revised application pending.)

More generally, we believe there is significant potential for this work to be of interest to the real estate industry, not just in academic circles, especially if a sentiment series could be generated on an ongoing basis. We are already in dialogue with UK CRE news suppliers about the project and we are now developing the relationship with pan-European news providers.

RREF is committed to supporting new research to enable the discovery of new solutions and insights, if you are interested in supporting research or discovering more about what projects are being supported t please contact us at [email protected] or on +44(0)118 378 4069